How Healthcare Trend Management Can Save Your County Millions

Dialing Back Costs – And Rangling “Trend”

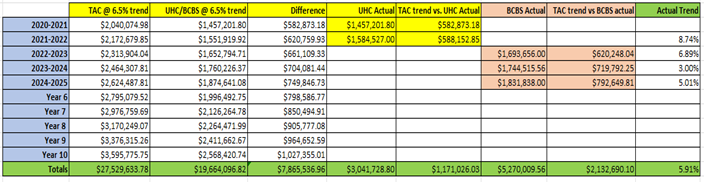

In 2020, we were brought on as healthcare consultants for a Texas County client, where we worked closely with the County Treasurer to assess their health insurance spending through the Texas Association of Counties (TAC) from 2009 to 2019. Over that decade, the County’s health insurance premiums increased at an average rate of 6.5% annually, with fluctuations ranging from 2% to 15% in certain years.

In their last year with TAC, the County’s gross annual premium for health insurance was $1,915,563.36, and was facing a renewal with TAC for 2020 that would have taken premiums above $2mm. To project future costs, we applied the historical trend of a 6.5% annual increase from 2020 onward.

However, by switching plans, we were able to deliver better benefits in 2020—lower deductibles, copays, and out-of-pocket expenses—while reducing the County’s annual premium down to $1,457,201.80 that year, a $582,873.18 savings in the first year alone.

In 2021-2022, if they had stayed with TAC and continued the 6.5% trend, their premiums would have reached $2,172,679.85. Instead, their annual premium was $1,551,919.92—which was a modest increase of 8.74% from the prior year but still significantly below TAC’s projected cost.

Looking ahead to current, 2024-2025, if the County had continued on with TAC, and continued to trend at 6.5%, their premiums would have soared to $2,624,487.81. Instead, they are slated to pay $1,831,838 in 2024-2025, $792,649.81 below where they would have been.

The savings delta is widening, and here’s why. Since transitioning into different strategies beginning in 2020, the County’s actual trend increase has been just 5.91% per year, compared to the 6.5% they previously experienced. Not only did the County cut costs in 2020, but we have also helped them reduce their annual premium trend rate.

Most notably, this County is still paying less in 2024-2025 than they were in 2019, with a current annualized premium of $1,831,838 compared to $1,915,563 in 2019. In total, since 2020, the County has saved approximately $3,303,716 in health insurance premiums by implementing better strategies and improving benefits for employees.

These savings are projected to compound over the decade from 2020-2030, with savings approaching $9mm by 2030.

Hiring an Independent Consultant

Texas Counties are allowed under Section 262.036 of the Local Government Code to hire independent benefits consultants/advisors “to obtain proposals and coverages for insurance”. These consultants are frequently called “Broker of Record” as well.

Sec. 262.036. SELECTION AND RETENTION OF INSURANCE BROKER. (a) Notwithstanding any other provision in this chapter, a county may select an appropriately licensed insurance agent as the sole broker of record to obtain proposals and coverages for insurance that provides necessary coverage and adequate limits of coverage in all areas of risk, including public official liability, property, casualty, workers' compensation, and specific and aggregate stop-loss coverage for self-funded health care.(b) The county may retain a broker of record selected under this section only on a fee basis paid by the county. A broker of record retained in this manner may not directly or indirectly receive any other remuneration, compensation, or other form of payment from any other source for the placement of insurance business under the broker of record contract.(c) A broker of record retained under this section may not submit any insurance carrier proposal to the county or direct any county insurance business to an insurance carrier if the broker has a business relationship or proposed business relationship with the carrier, including an appointment, unless the broker first discloses the nature of that relationship or proposed relationship, in writing, to the county.(d) A broker who violates this section is subject to any disciplinary remedy available under Chapter 82, Insurance Code, or Section 4005.102, Insurance Code, including license revocation and fine. Added by Acts 2005, 79th Leg., Ch. 353 (S.B. 1214), Sec. 1, eff. June 17, 2005.Amended by: Acts 2011, 82nd Leg., R.S., Ch. 285 (H.B. 1694), Sec. 16, eff. September 1, 2011.

Using an independent consultant can be a major benefit to a County. Independent consultants are different than “captive” agents, meaning they do not work for any insurer or entity in particular. This brings objectivity to the procurement process for Counties, and broadens access to multiple insurance solutions and strategies available in the market that the County may not have known about otherwise.

But pay close attention to the statute. A County may only select an independent consultant under specific criteria.

1) The broker of record/consultant can only work on a “fee basis”, meaning the consultant cannot earn revenues like “commissions” or any indirect remuneration from the insurance companies they are analyzing and ultimately recommending.

2) The broker of record/consultant must disclose in writing any direct or indirect relationships with insurers, including “appointments”.

These criteria are in place to eliminate real or perceived conflicts of interest. By removing any direct and indirect compensation the broker/consultant receives from insurers, it creates a direct relationship where the broker/consultant is fully-aligned with the interests of the County.

Additionally, independent consultants typically offer analyses to Counties in the areas of risk, claim spend and utilization, historical trend, benchmarking, and budget projection analysis. If your County is interested in learning more about ways to address healthcare costs without compromising the integrity of the benefits program, or how to engage with an independent healthcare consultant, we encourage you to reach out to us for more information.

testing testing

side bar

nav bar

widgget

Leave a Reply Cancel reply

You must be logged in to post a comment.