Inside TRS-ActiveCare: Subsidy, Erosion, and Deferred Deficits

TRS-ActiveCare: What the February 12, 2026 Board Materials Actually Reveal

On February 12, 2026, the Texas Retirement System (TRS) presented its annual health benefits update to the TRS Board. Beginning on page 141 of the February board book, TRS leadership walked through the financial condition, cost structure, and projected future of the TRS-ActiveCare health plan.

The materials are polished. The messaging is confident. But the data? Well, the data tells a much harder story.

Using only TRS’s own slides and projections, one conclusion is unavoidable: TRS-ActiveCare is not financially self-sustaining and survives only through recurring taxpayer subsidy and ongoing cost shifting to employees.

This is not my opinion. As you’ll see, it is reflected directly in the numbers TRS chose to present to it’s own board.

Employee costs have risen because the plan could not absorb them

One slide in particular deserves careful attention.

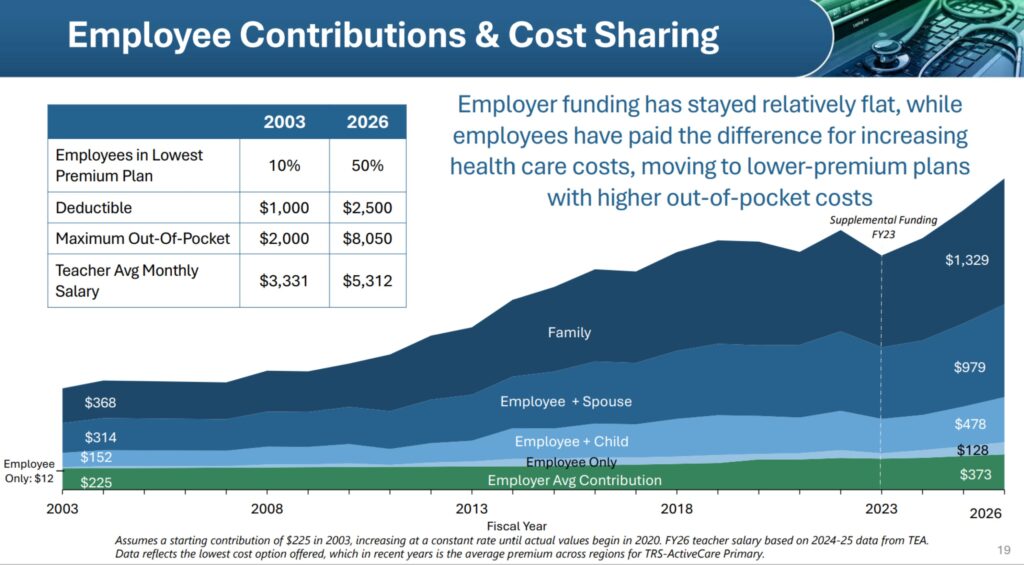

TRS explicitly states that employer funding has remained relatively flat while employees have absorbed rising health care costs by moving into lower-premium plans with higher out-of-pocket exposure. Here is TRS’s own language:

In 2003, only 10% of employees were enrolled in the lowest-premium plan. By 2026, that number has risen to 50%.

Over the same period, the deductible increased from $1,000 to $2,500. The maximum out-of-pocket limit rose from $2,000 to $8,050.

Not marginal changes. They represent a four-fold increase in financial exposure for employees who actually use their coverage.

TRS describes this as cost control. In reality, it is risk transfer.

Stability was achieved by making coverage worse, not by fixing the system

Supporters of TRS-ActiveCare often point to premium moderation as evidence of success. The February 12 presentation makes clear how that moderation was achieved.

Employees were pushed into cheaper plans. Deductibles rose. Out-of-pocket limits exploded. The plan became less protective, not more efficient.

That distinction matters…..a lot.

A plan that controls costs by improving care delivery, pricing discipline, and risk management looks very different from a plan that controls costs by exposing participants to higher financial risk. TRS-ActiveCare has followed the latter path.

The slide deck doesn’t even attempt to mask this. It actually documents it.

The fund balance depends on extraordinary taxpayer infusions

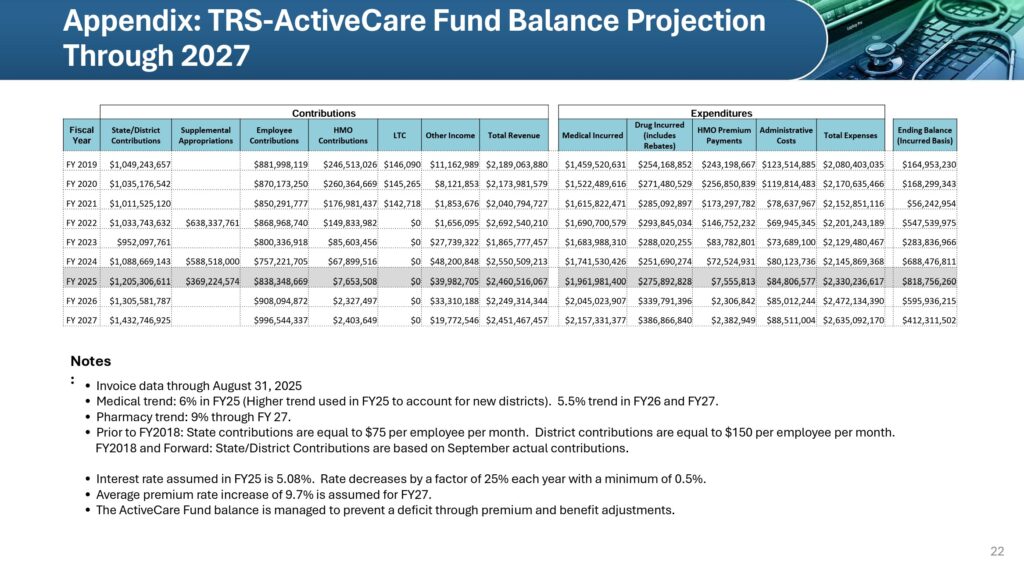

The appendix to the February 12 presentation includes the TRS-ActiveCare Fund Balance Projection through 2027.

The projection shows several years with positive ending balances. A closer look reveals why.

In fiscal years 2022, 2024, and 2025, the plan received hundreds of millions of dollars in supplemental appropriations. These infusions are the difference between reported surpluses and actual deficits.

Remove the supplemental funding, and those same years would have ended underwater.

A program that requires repeated, extraordinary appropriations to remain solvent is not self-supporting. It is purely subsidized. It’s not well managed, it’s bailed out time and again.

After subsidies taper, the deterioration is immediate

Even with prior infusions, the projection shows the fund balance declining sharply after fiscal year 2025.

Between 2025 and 2027, the ending balance falls by more than $400 million! It’s remarkable. Nearly half the fund balance disappears in two years.

This happens while medical costs continue to grow and pharmacy costs are projected to rise at a 9% annual trend.

That trajectory is not stable. It is deferred.

The projection quietly admits how deficits are avoided

Buried in the notes to the projection is one of the most important sentences in the entire presentation:

“The ActiveCare Fund balance is managed to prevent a deficit through premium and benefit adjustments.”

This is an explicit acknowledgment that when the math no longer works, the solution is not structural reform. The solution is to charge employees more or cover less…..or a combination of both of those.

That assumption is built into the projection itself. It is ASSUMING major premium hikes, worse benefits, and government bailout money.

The plan does not stabilize organically or through risk management. It is forced back into balance at the expense of teachers and tax payers.

This is a structural issue, not a temporary one

Taken together, the February 12 materials show a consistent pattern:

Costs rise faster than contributions.

– Employees absorb increasing financial risk.

– Taxpayers periodically inject large sums to prevent collapse.

– Future balance is preserved only by assuming premium increases and benefit reductions.

None of this is accidental. It is the predictable outcome of the way TRS-ActiveCare is designed and funded.

Programs built this way do not suddenly become self-sustaining. They require permanent intervention.

The takeaway

TRS-ActiveCare is often described as “stable”. The February 12, 2026 board materials show something else.

It is stable only because employees pay more and taxpayers step in when the numbers stop working.

That is not a judgment. It is a description of the system, using TRS’s own data.

Anyone evaluating participation in TRS-ActiveCare deserves to understand that reality clearly, before consequences become unavoidable.

testing testing

side bar

nav bar

widgget

Leave a Reply Cancel reply

You must be logged in to post a comment.